Mountain View Wealth ManagementArlington · Virginia

Financial Planning Guidance · (571) 368-6178

Honest answer: it depends — on more than any illustration will show you. Your timeline, your tax picture, and the simple truth that life rarely unfolds as planned: goals evolve, needs change, surprises arrive. The right decision is one that still fits when they do. Our complimentary buyer's guide walks through it all in plain English — the genuine strengths and the fine print, side by side.

Fixed indexed annuities are insurance contracts, not stock market investments. You do not directly participate in any index, and index-linked interest is limited by caps, participation rates, or spreads. Guarantees are backed by the claims-paying ability of the issuing insurer. Not FDIC insured.

A plain-English, 15-minute read. Inside:

We will email the guide and nothing else unless you ask. No obligation, no sales calls from a submission. See disclosures below.

In years the index falls, credited interest is 0% — your contract value doesn't decline from index losses. Rider fees and early surrender are the exceptions worth understanding.

You receive part of the index's gains, defined by caps, participation rates, or spreads — and typically excluding dividends. The formula, not the market, is what you're buying.

Surrender schedules often run 7–10 years. Carriers can typically reset caps and participation rates each term. Optional income riders charge annual fees even in 0% years.

A hypothetical contract with a 7% cap, annual point-to-point crediting. Illustrative only — caps vary by contract and can change at renewal.

The cap limits the credit. The 5-point difference is the cost of the floor.

Below the cap, the credit matches the index gain (excluding dividends).

The floor holds at 0%. Note: rider fees, if elected, are still deducted.

Hypothetical example for education only; not a prediction or an offer of any product. Actual crediting depends on the specific contract's method, terms, and renewal rates.

A short fit check below — so we only book time that's worth yours.

We'll send a one-page checklist: recent statements, existing annuity contracts or any FIA illustration you've been shown elsewhere, your Social Security estimate.

A working session, not a pitch — plan for one to two hours, thorough rather than rushed. You leave knowing whether an FIA fits your plan, and second opinions on proposals you've received are welcome.

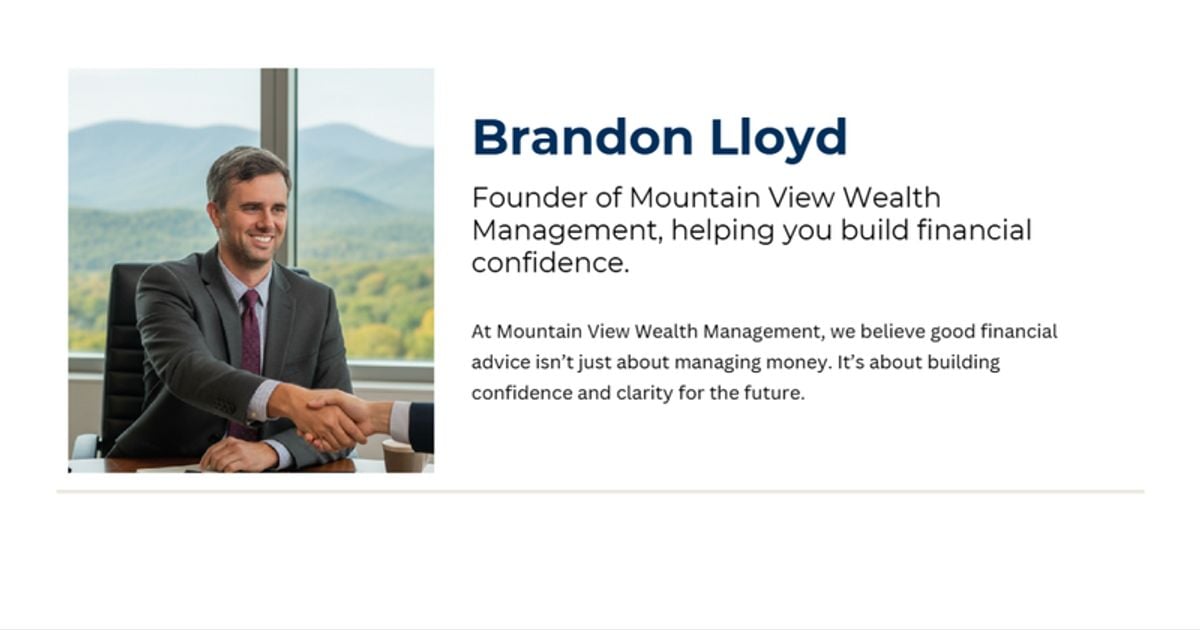

Founding Partner & President, Mountain View Wealth Management

Brandon began his career in private equity in 2010 and went on to Wells Fargo Advisors before founding Mountain View Wealth Management in Arlington. He is a CERTIFIED FINANCIAL PLANNER™ professional and holds a B.S. in Finance from James Madison University.

His approach to annuity questions is the same as the firm's approach to everything else: the recommendation comes after the full picture — which is why every working session starts with your statements on the table, not a product brochure.

A complimentary working session — your full picture, honestly assessed.

Savings, brokerage, and retirement accounts — excluding your home.

A real one — income, taxes, investments, and estate working together.

Gut answer is the honest one.

Either answer is fine — it just shapes the meeting.

Choose a time below. Your confirmation email will include this checklist — bringing it makes the meeting genuinely useful:

Working session · typically one to two hours · 2611 S Clark St., Suite 600, Arlington, VA 22202

Prefer to schedule by phone? (571) 368-6178

Based on your answers, we'd suggest starting with our buyer's guide rather than an office meeting — it will answer most first-stage questions. If your situation changes, we're here.

Start with the buyer's guide on your own time. The ten questions at the back will serve you in any annuity conversation, with us or anyone else. If you change your mind, this page will be here.